Quick Answer:

The chargeback process starts when a cardholder disputes a charge with their bank and ends 30–90+ days later with a decision. The merchant has a limited window (typically 20–45 days depending on the card network) to respond with evidence.

Time limits: Visa gives cardholders 120 days to file. Mastercard gives 120 days. Merchants then have 20–30 days to respond. The entire process from dispute to resolution takes 30–90+ days.

Simply put: The chargeback timeline is long, stressful, and expensive. Every stage has a deadline. Missing one means you automatically lose.

Key Takeaways

- The chargeback process has 5 stages: dispute filed, bank investigation, merchant notification, representment, and resolution. You only control one of them — representment.

- Visa and Mastercard chargeback time limits give cardholders 120 days from the transaction date (or expected delivery date) to file a dispute. After that window closes, no chargeback can be filed.

- Merchants typically have 20–30 days to respond with evidence. Missing this deadline means you automatically lose — no exceptions.

- The chargeback process flow generates fees at every stage: chargeback fee ($25–$100), processing fee (not refunded), and potential arbitration fee ($500+) if the dispute escalates.

- Prevention at every stage is cheaper than fighting. Alert services can intercept disputes before they become chargebacks. Issuing a refund is cheaper than the chargeback process. See our chargeback prevention guide.

How Does a Chargeback Work?

A chargeback is a forced reversal of a credit or debit card transaction. Instead of asking the merchant for a refund, the cardholder contacts their issuing bank and disputes the charge. The bank then reverses the transaction, pulling funds from the merchant’s account.

The chargeback process involves five parties: the cardholder (customer), the issuing bank (customer’s bank), the card network (Visa, Mastercard, Amex, Discover), the acquiring bank (merchant’s bank), and the merchant. Each party has specific roles, timelines, and responsibilities.

Here’s how the entire chargeback process flow works, stage by stage:

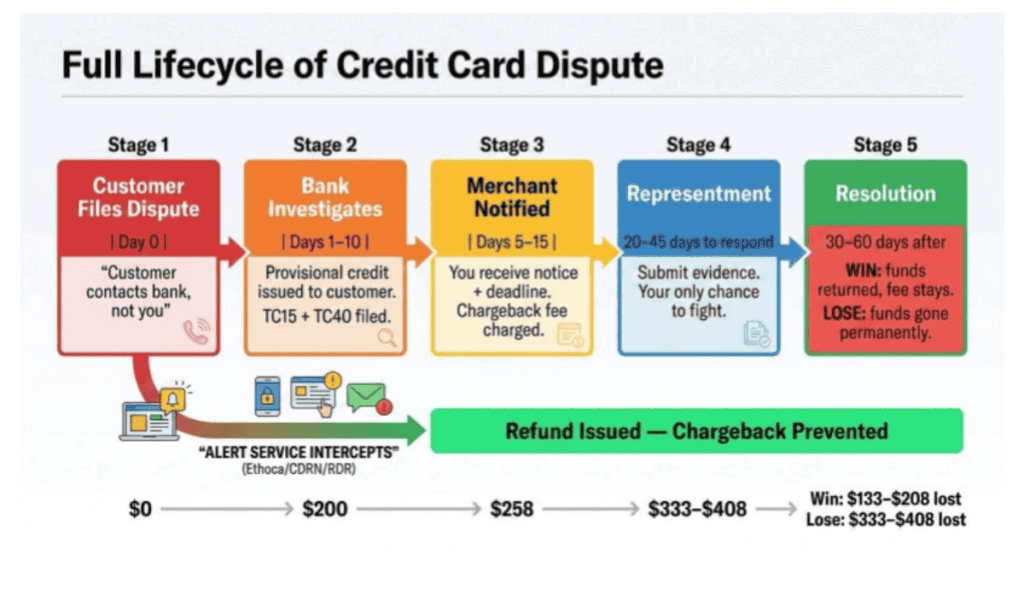

Stage 1: The Customer Files a Dispute

Timeline: Day 0

The chargeback process starts when the cardholder contacts their issuing bank to dispute a charge. The customer tells the bank they don’t recognize the charge, didn’t authorize it, never received the product, or aren’t satisfied with what they received.

The bank assigns a chargeback reason code based on the customer’s claim. This code determines the evidence requirements for the entire dispute. Common reason codes include Visa 10.4 (card-not-present fraud), Visa 13.1 (merchandise not received), Mastercard 4837 (no cardholder authorization), and Mastercard 4853 (cardholder dispute).

What you can do at this stage: Nothing — you don’t know about it yet. This is why chargeback prevention matters: alert services like Ethoca, Verifi CDRN, and Order Insight can notify you at this stage, giving you 24–72 hours to issue a refund before the dispute becomes a formal chargeback.

Stage 2: The Issuing Bank Investigates

Timeline: Days 1–10

The issuing bank reviews the customer’s claim and decides whether the chargeback is valid. For fraud claims, the bank checks whether the transaction passed security verification (AVS, CVV, 3D Secure). For product disputes, they review the customer’s description of the problem.

If the bank determines the dispute has merit, they issue a provisional credit to the cardholder — the customer gets their money back immediately. This provisional credit is taken from the merchant’s acquiring bank, which then debits it from the merchant’s account.

At this point, the issuing bank also files the relevant network alerts: a TC15 dispute alert and, for fraud-related claims, a TC40 fraud report. Both of these count toward your Visa VAMP ratio.

What you can do at this stage: If you received an alert from Ethoca, CDRN, or RDR during Stage 1, you can still issue a refund to prevent the formal chargeback. Once the bank has issued the provisional credit, the chargeback is official.

Stage 3: The Merchant Is Notified

Timeline: Days 5–15

Your acquiring bank or payment processor notifies you of the chargeback. You’ll receive details including the transaction amount, the reason code, the cardholder’s claim, and a deadline for your response.

At this point, the chargeback fee ($25–$100) is charged to your account regardless of the outcome. Even if you win the dispute, the chargeback fee is not refunded. See our high-risk merchant account fees guide for typical fee ranges.

What you should do immediately:

- Record the deadline — missing it means automatic loss

- Review the reason code to understand what evidence is required

- Start gathering evidence (more on this below)

- Decide whether to fight or accept the chargeback based on your evidence and the dollar amount

Running Cost Calculator: What a $200 Chargeback Actually Costs You

As the chargeback moves through each stage, costs compound. Here’s a running total for a $200 disputed transaction on a high-risk merchant account:

Stage | What Happens | Running Total |

Stage 1 | Customer disputes. You don’t know yet. | $0 (so far) |

Stage 2 | Bank issues provisional credit. $200 debited from your account. | $200 |

Stage 3 | You’re notified. Chargeback fee ($50) charged. Original processing fee ($8 at 4%) not returned. | $258 |

Stage 4 (if you fight) | 2–4 hours of work gathering evidence, writing rebuttal. Estimated at $75–$150 in labor. | $333–$408 |

Stage 5 — YOU WIN | $200 transaction returned to you. But you still paid the $50 fee + $8 processing fee + labor. | Net loss: $133–$208 |

Stage 5 — YOU LOSE | $200 gone permanently + $50 fee + $8 processing fee + labor + ratio damage. | Net loss: $333–$408 + ratio |

If you had issued a refund instead | $200 returned to customer. No fee, no ratio damage, 5 minutes of work. | Net loss: $200 |

The math is clear: even when you WIN a chargeback, it costs you $133–$208 on a $200 transaction. When you lose, it’s $333–$408. A refund would have cost $200 with zero ratio damage and 5 minutes of work.

This is why chargeback prevention is always cheaper than fighting chargebacks after the fact.

Your 48-Hour Chargeback Action Plan

When you receive a chargeback notification, here is exactly what to do:

Hour 1 — Record and assess. Write down the response deadline. Look up the reason code and understand what evidence is required. Pull up the original order in your system using the transaction ID.

Hours 2–4 — Gather evidence. Pull shipping tracking and delivery confirmation. Screenshot the order page, product description, and terms the customer agreed to. Export customer communication logs (emails, chat transcripts, support tickets). Pull AVS/CVV verification results and 3D Secure authentication records. Check if this customer has prior successful orders (potential CE 3.0 candidate).

Hours 4–8 — Decide: fight or accept. Do you have evidence that directly addresses the reason code? Is the dollar amount worth 2–4 hours of representment work? Is your chargeback ratio in a safe zone or approaching 1%? If your evidence is weak and the amount is small, accepting the loss saves time — but the chargeback still counts against your ratio either way.

Day 1 — Draft your rebuttal. Write a clear, factual rebuttal letter that addresses the specific reason code. Attach all supporting evidence. Do not be emotional or argumentative — the bank reviewer reads hundreds of these. Be concise and make the evidence easy to follow.

Day 2 — Submit. Review your rebuttal package for completeness, then submit through your processor’s dispute portal. Confirm receipt. Save a copy of everything. Then wait — the bank takes 30–60 days to review and decide.

Ongoing — Track and learn. Log every chargeback in a spreadsheet: date, amount, reason code, whether you fought it, and the outcome. After 3–6 months, patterns emerge — you’ll see which reason codes hit you most and can target your prevention effort saccordingly.

Stage 4: Representment (Your Response)

Timeline: You have 20–45 days from notification (varies by network)

Representment is your opportunity to fight the chargeback by submitting evidence proving the transaction was legitimate. This is the only stage of the chargeback process where you have any control over the outcome.

For detailed guidance on building a strong representment case, see our guide on how to dispute chargebacks as a merchant.

Evidence to gather based on reason code:

Fraud claims (Visa 10.4, Mastercard 4837): AVS/CVV verification results, 3D Secure authentication records, IP address and device fingerprint matching the customer’s prior transactions, delivery confirmation with signature, login/usage records after purchase.

Product not received (Visa 13.1, Mastercard 4855): Shipping tracking showing delivery to the correct address, delivery confirmation with signature, carrier GPS data, customer communication acknowledging receipt.

Not as described (Visa 13.3, Mastercard 4853): Product page screenshots, accurate product descriptions, photos of the actual product, terms of service, refund policy the customer agreed to.

Cancelled recurring (Visa 13.2, Mastercard 4841): Proof that the customer did not cancel before the charge date, cancellation policy they agreed to, usage records showing continued access after the disputed charge.

Compelling Evidence 3.0: For Visa 10.4 fraud disputes, CE 3.0 lets you submit data from two prior undisputed transactions with the same customer. If at least two of four data elements match (IP, device ID, shipping address, user ID), Visa removes the TC40 from your VAMP numerator and you keep the revenue.

Submit your evidence package — called a rebuttal letter — to your acquiring bank or processor before the deadline. Include only evidence relevant to the specific reason code. Submitting irrelevant evidence wastes the reviewer’s time and weakens your case.

Stage 5: Resolution

Timeline: 30–60 days after representment

The issuing bank reviews your evidence and makes a decision:

If you win: The provisional credit is reversed. The cardholder’s account is debited, and the funds are returned to your merchant account. You still pay the chargeback fee, but you keep the transaction amount.

If you lose: The provisional credit becomes permanent. The customer keeps the money, you lose the transaction amount plus the chargeback fee, and the dispute counts against your chargeback ratio.

Pre-arbitration / arbitration: If either party disagrees with the decision, the dispute can be escalated to the card network for final arbitration. This is rare (less than 5% of chargebacks reach this stage) and expensive — arbitration fees run $250–$500+ and are charged to the losing party.

Average merchant win rate on representment is 30–45%. With strong evidence and the correct response to the specific reason code, win rates can reach 60–70%.

Chargeback Time Limits by Card Network

Every card network has different time limits for filing chargebacks, responding, and resolving disputes. Missing any deadline means you lose by default.

Visa | Mastercard | Amex | Discover | |

Customer filing window | 120 days | 120 days | 120 days | 120 days |

Merchant response window | 30 days | 45 days | 20 days | 30 days |

Pre-arbitration window | 30 days | 45 days | N/A | 30 days |

Arbitration window | 10 days | 45 days | N/A | 30 days |

Total process | 60–90+ days | 60–90+ days | 45–75 days | 60–90+ days |

Note: Filing windows start from the transaction date or the expected delivery date, whichever is later. For recurring transactions, the window starts from the date of the disputed charge, not the original subscription start date. Times are calendar days, not business days.

Visa chargeback time limit: Cardholders have 120 days to file. Merchants have 30 days to respond. The Visa chargeback time frame from start to resolution is typically 60–90 days.

Mastercard chargeback time frame: Cardholders have 120 days to file. Merchants have 45 days to respond — the longest response window of any network. The Mastercard chargeback timeframe from start to resolution is typically 60–90 days.

Debit card chargeback time limit: Debit card chargebacks follow the same network rules as credit cards (Visa debit = Visa rules, Mastercard debit = Mastercard rules). However, debit chargebacks are governed by Regulation E, which requires the bank to investigate within 10 business days for provisional credit.

What Happens If You Don’t Respond to a Chargeback

If you miss the representment deadline or choose not to respond:

- You automatically lose the dispute

- The customer keeps the refunded money permanently

- You still pay the chargeback fee ($25–$100)

- The dispute counts against your chargeback ratio

- It counts toward your VAMP ratio (TC15 + potentially TC40)

There is no benefit to ignoring a chargeback. If you have any evidence at all, respond. If you don’t have evidence, the chargeback is still counted against your ratio whether you respond or not — so you lose nothing by trying.

How to Speed Up Chargeback Processing

You can’t control the bank’s timeline, but you can control how fast you respond:

Set up real-time chargeback notifications. Most processors can email you instantly when a chargeback is filed. Don’t rely on monthly statements to discover disputes.

Pre-build evidence templates. Create response templates for your most common reason codes (10.4, 13.1, 13.3, 4837, 4853). When a chargeback hits, you fill in the transaction-specific details instead of starting from scratch.

Automate evidence collection. Configure your payment gateway, CRM, and shipping system to store all relevant data in one place. When you need to respond, everything is already organized.

Use chargeback alert services. Ethoca, Verifi CDRN, Order Insight, and RDR can intercept disputes before they become chargebacks. See our chargeback alerts guide.

Respond within 48 hours. Even though you may have 30–45 days, responding quickly shows the bank you take disputes seriously and have your evidence organized.

Frequently Asked Questions

A chargeback works in 5 stages: the customer files a dispute with their bank, the bank investigates and issues a provisional credit, the merchant is notified and given a response deadline, the merchant submits evidence (representment), and the bank makes a final decision. The entire chargeback process takes 30–90+ days.

From dispute to resolution, a chargeback takes 30–90+ days. The customer has up to 120 days to file. The merchant has 20–45 days to respond (depending on the card network). The bank then takes 30–60 days to review and decide. If escalated to arbitration, add another 30–45 days.

Cardholders have 120 days to file a chargeback from the transaction date or expected delivery date. Merchants have 20–45 days to respond after notification. The Visa chargeback time limit is 120 days for filing and 30 days for merchant response. The Mastercard chargeback time limit is 120 days for filing and 45 days for response.

The chargeback process flow is: Customer disputes charge → Issuing bank investigates → Provisional credit issued to customer → Merchant notified with reason code and deadline → Merchant submits evidence (representment) → Bank reviews and decides → Funds returned to merchant (win) or kept by customer (loss). Optional: pre-arbitration and arbitration if either party disagrees.

Cardholders have 120 days from the transaction date (or expected delivery date) to file a chargeback with their issuing bank. For recurring charges, the window starts from the date of the specific disputed charge. After 120 days, the chargeback window closes and the transaction is final.

Mastercard gives cardholders 120 days to file a chargeback and merchants 45 days to respond with evidence — the longest merchant response window of any card network. The Mastercard chargeback time frame from start to resolution is typically 60–90 days. Pre-arbitration adds 45 days, and arbitration adds another 45.

Debit card chargebacks follow the same network time limits as credit cards (Visa debit = 120 days to file, Mastercard debit = 120 days). However, debit chargebacks are also governed by Regulation E, which requires the issuing bank to investigate within 10 business days and issue a provisional credit.

Yes. Chargeback alert services (Ethoca, Verifi CDRN, Order Insight, RDR) notify you when a customer begins a dispute, giving you 24–72 hours to issue a refund insteadand prevent the formal chargeback. For comprehensive prevention strategies, see our chargeback prevention guide.

Don’t Let the Chargeback Process Drain Your Business

Every chargeback that goes through the full process costs you 2–4 hours of work, $25–$100 in fees, and damage to your chargeback ratio — with only a 30–45% chance of winning. Prevention is faster, cheaper, and more reliable.

DirectPayNet helps high-risk merchants set up chargeback prevention and management that catches disputes before they enter the formal chargeback process. Alert services, representment support, and ratio monitoring — all managed for you.